New Temporary Tax Reliefs on Qualifying Capital Asset Investments from 1 April 2021

We have received several queries since the announcement on Budget Day on what the new temporary tax reliefs mean for businesses. Below we have answered some helpful questions.

I am a sole trader, can I avail of the super-deduction?

The super-deduction is only available to limited companies.

When does the expenditure qualify?

Expenditure incurred after 1 April 2021 will qualify. There may be exclusions for contracts entered into prior to 3 March 2021.

What assets will qualify?

- Main rate assets cover the majority of plant and machinery. New main rate assets will qualify for the 130% super-deduction subject to certain exclusions.

- Special rate assets include assets such as integral features of buildings and long-life assets. Special rate assets will qualify for the 50% special rate first-year allowance subject to certain exclusions.

- Cars will not qualify for the super-deduction.

- Used or second-hand assets will not qualify for the super-deduction.

- Assets bought on Hire Purchase or similar contract must meet additional conditions to qualify for the super-deduction and special rate relief.

- That you are paying a periodical sum and in return plant and machinery assets are hired to you;

- that eventually you can end up owning those assets;

- that the person who hires/receives the goods is the one incurring the expenditure (i.e. paying for the contract). This makes sure that the benefit of the deduction goes to the business rather than the lender.

Do I have to claim the super-deduction, or can I claim the Annual Investment Allowance?

Companies can claim a combination of the super-deduction for main rate or 50% FYA for special rate and the AIA ( up to £1m at 100% first year allowance ) on all qualifying assets.

Utilising the super-deduction does not reduce the level of AIA available for other capital expenditure that does not qualify for the super-deduction.

However, there can be no double claiming i.e., a claim to the AIA and the super-deduction on the same expenditure.

What happens when I come to sell an asset I have claimed the super-deduction on?

Disposal receipts should be treated as balancing charges (taxable profits), instead of being taken to capital allowances pools.

This is subject to adjustments if a company did not previously claim its full entitlement to the relevant new allowance or if some of the expenditure on the asset was subject to other allowances.

This applies to both the super-deduction and the 50% first-year allowance for special rate assets.

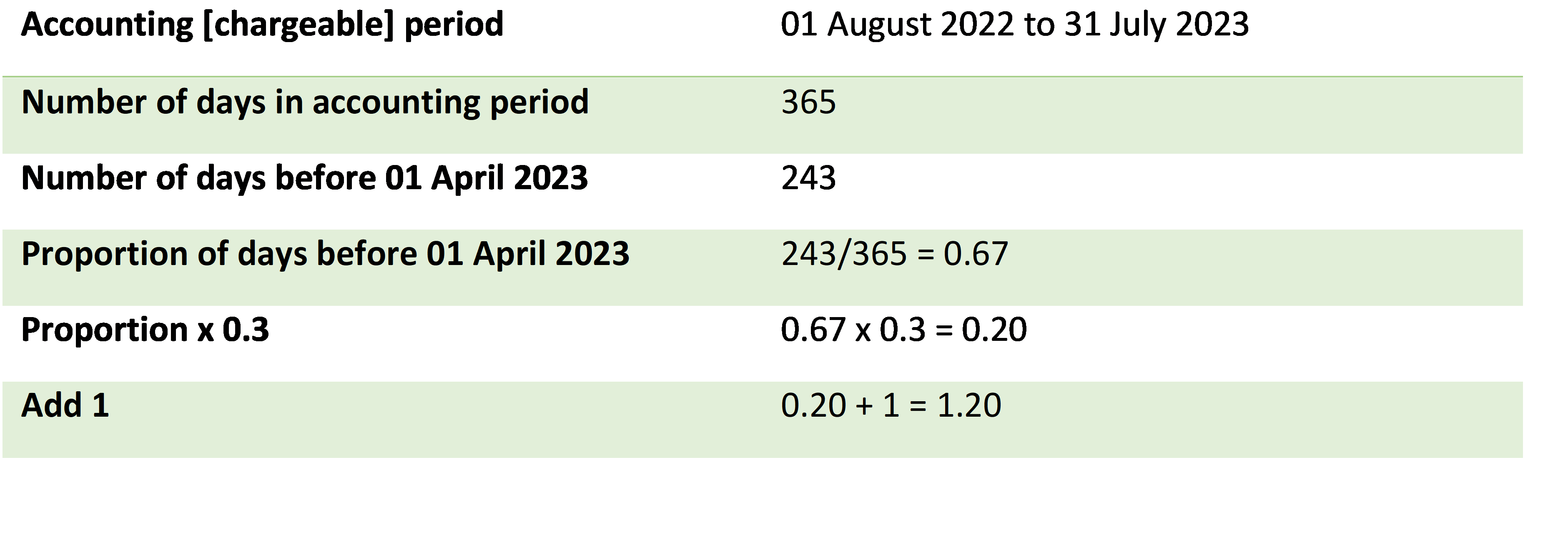

For the super-deduction disposals are multiplied by a factor of 1.3 for accounting periods ending prior to 1 April 2023, so anything disposed of in the qualifying period has the potential to be fully clawed back.

A time apportionment rule will apply to the factor for accounting periods that commence before 1 April 2023 but end on or after that day. For example:

There is some high-level guidance on gov.uk and HM Treasury has published a factsheet on the super-deduction which may be helpful.

If you have any queries, please contact our Tax team.

_2.jpg)

Whilst every effort has been made by CavanaghKelly to ensure the accuracy of the information here, it cannot be guaranteed and neither CavanaghKelly nor any related entity shall have liability to any person who relies on the information herein. Information given here is for guidance only. Detailed professional advice should be taken before acting on any information contained herein. If having read the guidance here, you would like to discuss further; a member of our team would be pleased to help you.