Company Cars - Beware the road ahead

You are thinking about investing in a new car but as a business owner, what's the best option for you? Investing in company cars can be expensive so it's important to look for the most cost effective and tax efficient way to do it.

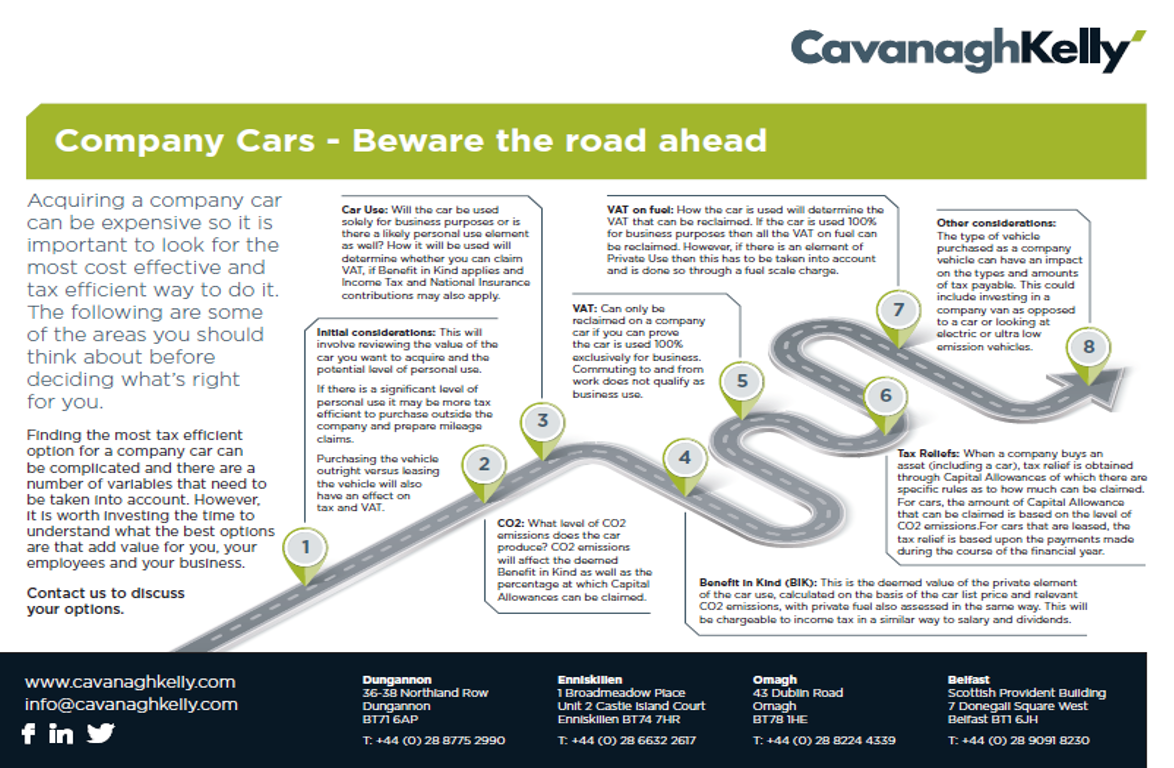

A PDF information sheet is available to download here.

Do you purchase the car personally or through the company? Can you reclaim VAT? What are Benefits in Kind? Is the type of car important?

When deciding how to fund your purchase, the first questions to ask are:t are Benefits in Kind? Is the type of car important?

- How will the car be used: solely business use or also private use?

- What level of CO2 emissions does the car?

If the vehicle is for 100% Business Use then you can claim VAT, but if the vehicle has a Private Use element then Benefit in Kind may come into play in which case you may have to pay Income Tax and also Class 1A National Insurance.

The CO2 emissions produced by the car will also directly affect the deemed Benefit in Kind on which you will be taxed and the percentage at which Capital Allowances can be claimed on the vehicle expenditure.

There are a lot of variables to think about. The following looks at the some of the key considerations in more detail and uses working examples to allow you to start to think about which option may make the most sense for you in terms of your business and your tax bill. All Rates and Allowances in this article are based on the 2018 / 2019 tax year.

VAT

VAT can only be reclaimed if the company car is 100% exclusively for Business Use. You must prove to HMRC that it is not available for Private Use by you or your employees e.g a pool car that is kept on business premises overnight and is readily available for more than 1 employee for business purposes throughout the business working day.

Other exemptions which allow VAT to be reclaimed include:

- Used primarily for taxi

- Used for driving instruction

- Used for self drive

NOTE: driving to and from work is known as your 'ordinary commute' and does not qualify as Business Use by HMRC. Therefore, even if the car is used only to travel to and from work, VAT cannot be reclaimed.

Benefit in Kind

Benefit in Kind (BIK) is a benefit or expense that employees or directors receive as part of their employment but is not included in their salary or wages. Employers providing BIK may need to inform HMRC and pay tax or National Insurance on it. There are different rules for what employers have to report and pay depending on the type of expense or benefit provided. Company cars, company vans and fuel can be included as BIK. Every vehicle has a BIK percentage banding. This is based on CO2 emissions, P11D value (list price including extras) and VAT, but excluding the first year registration fee and vehicle tax.

When looking at a company car as BIK you need to take into consideration the amount of tax you pay as well as the type of vehicle it is.

Let’s take a look at an example:

| Vehicle | VW Golf S 1.6 TDI | |

| List Price | £21,355 | |

| CO2 emissions | 106 g/km | |

|

In this example the CO2 emissions percentage per HMRC is 26%, so the taxable benefit will be: £21,355 x 26% = £5,552.30 NOTE: this is the taxable benefit, not the actual amount of tax you will pay. |

||

Fuel

Whether the fuel is being used for business or private use will determine level of taxable benefits available.

Private Use

If fuel is provided to an employee for private use, then the employee is deemed to be receiving a Benefit in Kind. It is therefore a taxable benefit and will be based on the CO2 emission percentage multiplied by £23,400.

Using the previous example of the Golf:

| Vehicle | VW Golf S 1.6 TDI | |

| CO2 emissions | 106 g/km | |

|

The Benefit in Kind percentage has been calculated at 26% so the taxable benefit for fuel for Private Use would be £23,400 x 26% = £6,084 NOTE: the £23,400 is a fixed amount regardless of how much fuel is actually being provided to the employee for Private Use. |

||

Fuel that Employees pay for

You don’t have to pay or report on fuel, including for private journeys, if employees buy the fuel for their own use or the employer buys it and the employee pays it back during the tax year and their payment is equal to or more than the amount the employer originally paid.

Business Use

If fuel is provided solely for Business Use there is no Benefit in Kind payment and so no additional tax to be paid. However, it is essential that there is proof that no fuel was used for Private Use. This can be achieved through keeping records of accurate mileage or by payments made to the company by the employee for any non-business use. Also the condition of ‘ordinary commute’ applies i.e the commute to and from work does not qualify as Business Use.

VAT on Fuel: Business Use v Private Use

If fuel is provided by the company solely for Business Use then all of the VAT on fuel can be reclaimed.

If the fuel is provided by the company and is used for Private Use, then the Private Use has to be taken into account and is done so through a fuel scale charge. In this instance, the Company can reclaim all of the VAT on the fuel and then they are required to pay the appropriate fuel scale charge back to HMRC to cover the Private Use element. This charge is based on CO2 emissions of the vehicle.

Using our working example and the fuel scale charges for the 2018/2019 tax year:

| Vehicle | VW Golf S 1.6 TDI | |

| CO2 emissions | 106 g/km | |

| If fuel used for Private Use is paid for in full by the Company with all the VAT being reclaimed, the quarterly fuel scale charge to be added on to the total VAT liability would be £23.33 per quarter. | ||

Are there exemptions to BIK payments?

If the car or fuel is provided as part of a salary sacrifice arrangement then it must be reported to HMRC. Scenarios where providing a car / fuel may not need to be reported to HMRC include:

- Privately owned cars

- Cars available for business journeys only (i.e. part of your employee’s duties or that an employee has to make to get to a temporary workplace)

- Cars adapted for an employee with a disability (This includes cars with an automatic transmission if the employee’s disability requires this. The cars are exempt if the only private use is for journeys between home and work and travel to work related training.

- Fuel that employees pay for:

- Pool cars: cars that are shared by employees for business purposes and normally kept on business premises are exempt from BIK. However, payment is required if the pool car is driven for private use or if the car is shared by employees but does not qualify as a pool car.

- Cars provided to close relatives (spouse or civil partner; son or daughter and their spouse or civil partner; your parents; any other dependants or guest of your household) Payment is not required if the following conditions are met:

- The employer is an individual e.g. a sole trader

- The employer is providing the car to someone who works in the business but only because they are a close relative and not because they work for the employer (e.g. a car is given to a child as a birthday present).

Capital Allowances

When a company buys an asset (including a car) it is not treated as a deductible expense. Tax relief is obtained through Capital Allowances and there are specific rules regarding how much can be claimed. For cars, the amount of Capital Allowance that can be claimed is based on the level of CO2 emissions produced so in broad terms, the more CO2 the car produces, the less you can claim in tax relief. There are three bands that apply for CO2 levels:

- CO2 emissions 75g/km or less: 100% of the price of the car can claimed in the first year, but the car must be a new car

- CO2 emissions between 75g/km and 130g/km: Capital Allowance can be claimed at 18% per annum

- CO2 emission levels above 130g/km: Capital Allowance rate is 8% per annum

| Vehicle | VW Golf S 1.6 TDI |

| CO2 Emissions | 106 g/km |

|

In this example the CO2 emissions fall into the second band so Capital Allowances would be claimed at 18% per annum. |

|

Other Considerations

The kind of vehicle you invest in can have an impact of the type and amount of tax payable e.g. there can be a difference to how company car tax is applied to a company car versus a company van. Also, electric vehicles used to be exempt from BIK rules and were seen as a good tax efficient option. However, as of the 2016/2017 tax year there is now a requirement to report on zero emission vehicles. Whilst reporting is now a requirement, the BIK is paid at a reduced rate.

Finding the most tax efficient option for a company car is complicated and there are a number of variables that have to be taken into account. However, it is worth investing the time to see what the options are for you and your employees.

Get in touch with us to discuss the best options for your situation.

Whilst every effort has been made by CavanaghKelly to ensure the accuracy of the information here, it cannot be guaranteed and neither CavanaghKelly nor any related entity shall have liability to any person who relies on the information herein. Information given here is for guidance only. Detailed professional advice should be taken before acting on any information contained herein. If having read the guidance here, you would like to discuss further; a member of our team would be pleased to help you.