New Taxation Rules for Residential Landlords

As of 6 April 2016, the government made changes to the way landlords will be taxed on their rental profits from residential properties in the UK. Under the new rules, residential landlords will be no longer able to fully claim tax relief on the mortgage interest payments. The introduction of the finance cost restriction will gradually be phased in over a period of four years, starting from 6 April 2017.

The finance cost reduction will restrict the interest previously claimed on:

- Mortgages

- Loans, including loans to buy furnishing for the property

- Overdrafts

The new retrictions, will affect those who let residential properties either as:

- An individual

- A partnership

- As a trust

The restriction will not however affect commercially let properties, rentals properties held in a limited company and landlords of Furnished Holiday Lettings.

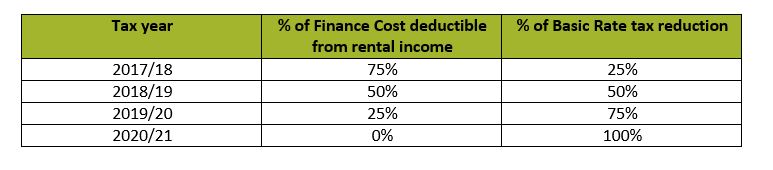

The restriction has been phased in gradually from 6 April 2017 and will be fully in place by 6 April 2020. Finance costs incurred will still be available for deduction when working out your taxable profits. However the finance deductions will be restricted each year and the remaining balance will be used to calculate your basic rate relief tax reduction.

Other factors to consider will be the affect that the new finance cost restriction will have on those who are claiming means tested benefits such as tax credits. Under the new rules, it may force individuals into the higher tax bracket and increase income which may result in them losing their tax credits.

Individuals who received Child Benefits, where their gross income previously was below the tax free limit of £50,000, under the new finance restriction rules, they may see their income increase over the tax free limit. This will result in a tax charge, and some of the child benefit may need to be paid back to HMRC.

The higher reported gross profit may also affect any means tested benefits such as Working Family Tax Credits, Student Finance and Educational Maintenance Allowances the tax payer may have traditionally availed of.

In addition, were an individual’s gross income was previously below £100K, under the new rules, their income may increase and therefore push them over the £100K mark. This will then result in the personal allowance being reduced and or potentially lost, result in higher taxable income.

There are a number of tax planning opportunities which may be available to individuals in order to reduce the tax burden from the new rules. However they may not be applicable in all situations and it is important to seek tax advice in advance of changing your individual structure.

If you wish to discuss the implications of the new finance cost reduction and how it will affect your tax liability or wish to obtain further advice on you own individual structure with regards to rental properties, please do not hesitate in contacting one of our team.

Whilst every effort has been made by CavanaghKelly to ensure the accuracy of the information here, it cannot be guaranteed and neither CavanaghKelly nor any related entity shall have liability to any person who relies on the information herein. Information given here is for guidance only. Detailed professional advice should be taken before acting on any information contained herein. If having read the guidance here, you would like to discuss further; a member of our team would be pleased to help you.